Perpetual vs. Periodic Inventory: What’s the Difference?

Reconciling accounting considerations with inventory convenience.

As children, many of us dreamed of running our own shops—whether a toy store or a confectionery. Running a retail business sounds fun... until you realize it's far more than sampling sweets or playing with toys all day.

Behind the scenes, you have to tackle less glamorous tasks, like inventory management and financial accounting. These two functions may seem separate, but they're closely connected. One helps track what you have, while the other tracks what it’s worth.

When it comes to recording inventory, most businesses use either a perpetual or periodic system:

• Periodic inventory updates them periodically, often through manual counts.

Let’s take a closer look at how these systems work—and which one makes sense for you.

Inventory Systems and the Role of Financial Accounting

To speak confidently on this topic, we need to dive into financial accounting. If you’ve never come across financial accounting before, the following concepts might feel a bit overwhelming. Don’t worry–we’ll take it step by step!

A Quick Look at the Accounting Basics

Financial accounting is the process of recording, summarizing, and reporting the financial activities of a business.

In the life of a small business owner, accounting can help clear up a lot of doubts related to money and inventory:

• How to determine if the new price offered by the supplier is within the company’s budget?

• Will there be enough money at the end of the year to pay employee bonuses?

At the core of the financial accounting system lies the general ledger.

The general ledger looks like a database or a spreadsheet. Most small businesses use accounting software (like QuickBooks or Xero) to manage their GL automatically. For example, when you pay a supplier through your bank account, this transaction is recorded in the GL in real time thanks to an integration with the bank application.

For our purposes, the most relevant components of the GL are:

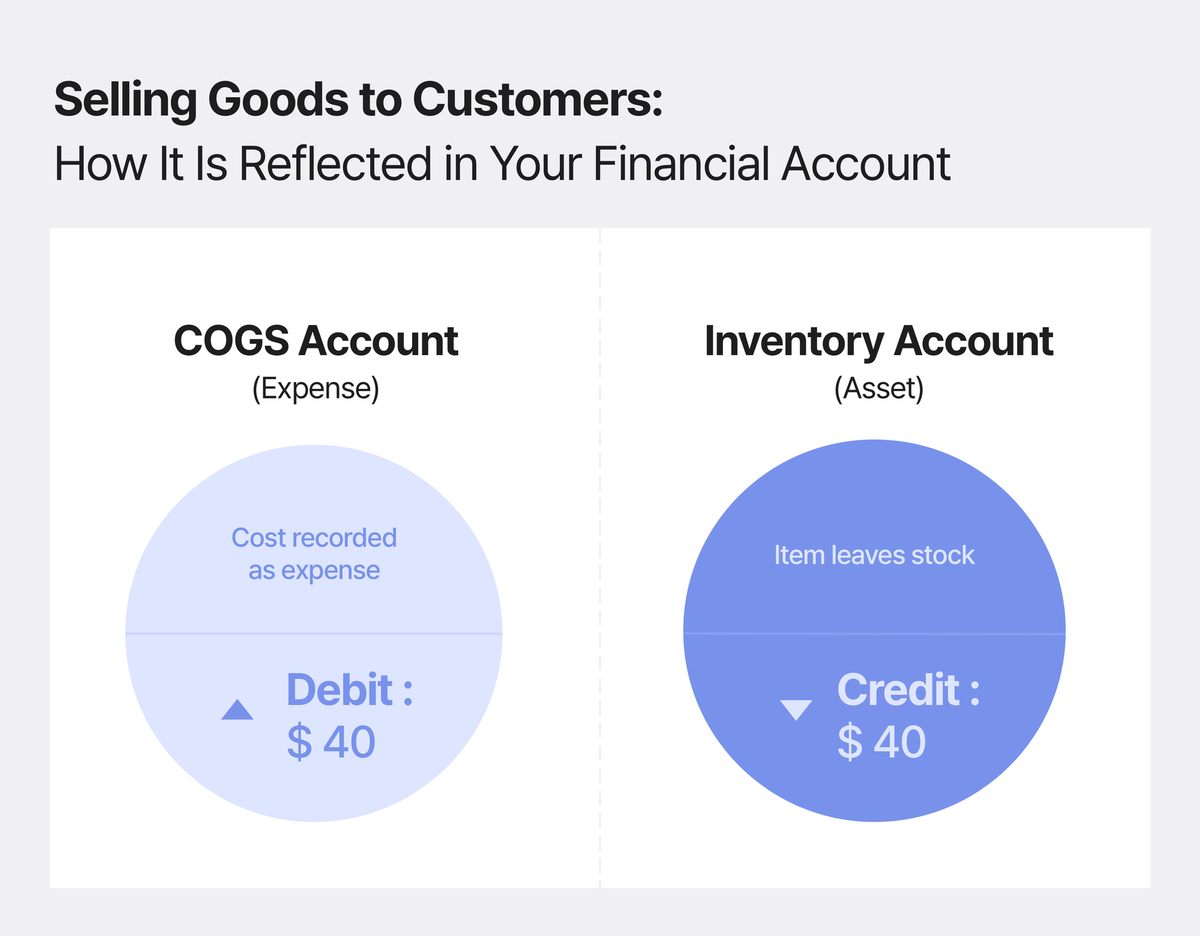

📌 COGS (Cost of Goods Sold) – Both a financial account and an important financial metric. It tracks how much the company paid for the items it has already sold.

For example, if you sell an item for $100 that originally cost $40, that $40 is recorded as COGS.

Now that we’re familiar with the general ledger and its main components, it’s time to connect the dots: How do these accounting concepts relate to periodic and perpetual inventory systems?

How These Accounts Work Together

Let’s say you sell an item from your inventory. As with any other transaction, this needs to be reflected in your financial account. But how exactly?

- The value of that item (i.e. cost) is moved out of the Inventory Account—because the item is no longer on hand.

- That same value is added into the COGS account—because you have now incurred the cost of selling that item.

This transfer reflects the fact that the inventory is no longer held by the company—it has (in accounting terms), become part of the cost required to generate revenue.

Now, this is where we’re getting close to our primary topic. How and when inventory and COGS are updated depends on the inventory system a business uses.

In other words, the periodic and the perpetual inventory systems differ in the way they recognize sold inventory.

The Perpetual System

In a perpetual system, the Inventory Account and COGS are updated in real time with each sale or purchase. This is made possible by tools like Point-of-Sale (POS) systems and ERP software.

In this system, the Inventory Account is credited, and COGS is debited at the moment of the transaction. Businesses will always have a current view of how much inventory they have on hand, and what their COGS is at any point in time.

The Periodic System

In a periodic system, inventory changes aren’t recorded in real time. Instead, businesses wait until the end of an accounting period (like monthly or quarterly) to calculate COGS and update the Inventory Account. COGS is calculated using the following formula:

COGS = Beginning Inventory + Purchases - Ending Inventory

Where

• Beginning Inventory: the amount on hand at the start of the period.

• Purchases: the total inventory bought during the period.

• Ending Inventory: the amount remaining, determined by a physical count.

Because there's no ongoing record of inventory, this system requires manual inventory counts, often at the end of the period, to know how much inventory is still in stock and how much was used or sold.

Once the physical count is done, COGS is debited based on the calculated amount and the Inventory Account is credited.

▶︎ A quick note on the role of manual counts:

We’ve mentioned cycle counting as a method for stock control and audit. Don’t get confused: in a perpetual inventory system, manual counts are done from time to time to make sure the virtual record matches what's actually in stock. But in a periodic inventory system, manual counts are not optional—they’re the only way to figure out how much inventory is left and to calculate the cost of goods sold.

So, while both systems may use manual counts, in the periodic system they are required, and in the perpetual system they are mainly for double-checking. Moreover, in a periodic inventory system, it's not possible to do random spot checks to prevent fraud or theft; there's no up-to-date inventory record to compare against.

▶︎ Why is COGS even important?

COGS directly reduces the gross profit and net income, since it reflects the direct cost of producing or purchasing the goods you sold. Understanding how costs flow from inventory to expenses is crucial for:

• Filing taxes properly

• Pricing items

• Managing supplier costs

• Planning cash flow

Getting COGS wrong can distort your financial statements. That’s why it’s so important to understand the difference between periodic and perpetual systems, and how they handle inventory and COGS.

Periodic vs. Perpetual Inventory: A Practical View

Let’s see how the two inventory systems differ in practice. We’ll walk through each system’s typical workflow, from the start to the end of a period. You’ll see how transactions are handled and when financial accounts are updated.

The Starting Point

Imagine you own a bookstore. At the end of the year 2024, you had 300 books in stock—you counted them all manually. You had purchased these books at $5 per book. Which brings us to an inventory value of $1,500 at the beginning of 2025.

Workflow 1: Periodic Inventory System

Beginning of 2025

Throughout 2025

Let’s say that you sell those books for $15 each.

At some point, you purchase 150 more books, at the same price of $5 per book, spending $750. This purchase is credited to a separate Purchases Account, not directly into inventory.

End of 2025

Following the count, you find 400 books remaining, with a total inventory value of $2,000.

▶︎ COGS Calculation

• Beginning Inventory = $1,500 (300 books at $5 each)

• Ending Inventory = $2,000 (400 books remaining at $5 each)

• Purchases = $750 (150 books at $5 each)

COGS = Beginning Inventory + Purchases - Ending Inventory

= 1,500 + 750 - 2,000 = $250

▶︎ General Ledger Update

COGS is recorded as a $250 expense in the income statement.

This inventory system is manual and retrospective, meaning you record and analyze inventory activity after it happens. It’s typically used by smaller businesses with lower transaction volumes or simple inventory needs.

Workflow 2: Perpetual Inventory System

Beginning of 2025

Throughout 2025

• Revenue is recorded immediately.

• Inventory Account is automatically reduced.

• COGS is simultaneously recorded in the General Ledger.

Real-Time Updates

End of 2025

For example:

• The system shows inventory valued at $2,000.

• Physical count reveals $1,822.

• A manual adjustment is made for the discrepancy.

This system is automated and real-time, which works well for businesses with high sales volume or multiple sales channels, especially when supported by inventory software or ERP systems.

Perpetual and Periodic Inventory Systems: The Differences

The periodic inventory system updates inventory and calculates cost of goods sold (COGS) only at the end of an accounting period. It relies on physical counts to calculate how much inventory is left at the end of the period.

In contrast, the perpetual inventory system tracks inventory and COGS continuously, with updates triggered by each transaction through barcode scans or point-of-sale systems.

|

Feature |

Periodic Inventory |

Perpetual Inventory |

|

COGS timing |

Calculated at end of period |

Updated continuously |

|

Inventory updates |

Manual, based on physical count |

Automatic, per transaction |

|

Physical count required? |

Yes, essential |

Optional (for reconciliation) |

|

Accuracy during the year |

Approximate |

High |

|

Complexity |

Simpler |

More complex / system-dependent |

While periodic systems are simpler, they offer less accuracy during the period. Perpetual systems require a robust back-end but provide real-time inventory visibility and more accurate financial reporting.

The Role of Technology in Inventory Accounting

One commonly cited advantage of a periodic inventory system is its low barrier to entry. It’s simple and cheap—you don’t need to purchase and then implement complex software. All it takes to get started is a team capable of performing basic inventory counts.

However, with today’s wide range of affordable and easy-to-use software solutions, this argument no longer holds as strongly. Technology has made real-time inventory tracking more accessible than ever, and tools like BoxHero are easily accessible to small businesses. They can:

- Import inventory data in bulk to generate unique barcodes.

- Scan items with a smartphone camera to register each transaction.

- View inventory updates from multiple staff or different warehouses

- Create custom fields or attributes to store specific item-level details.

- Integrate BoxHero with existing tools in their tech stack via the BoxHero API.

Perpetual vs. Periodic Inventory: How To Choose

We’ve discussed the accounting implications of the two systems above. Now, let’s consider which system actually fits your business.

▶︎ Inventory Size

Businesses with large, diverse, or fast-moving inventories typically benefit more from the real-time tracking capabilities of a perpetual system. For example, for a business giant like IKEA that manages tens of thousands of SKUS across global stores, it would be impractical to not track all sales in real time.

▶︎The Role of Inventory in Your Business Model

Additionally, if inventory is a central component of your business model, as in retail, manufacturing, or e-commerce, the real-time accuracy of a perpetual system can improve everything from purchasing to customer service.

But if inventory plays a smaller or more static role, a periodic system might be more sufficient and cost-effective.

▶︎Digital Readiness and Future Plans

If digital transformation is one of your strategic priorities, a periodic inventory system will simply hold you back, regardless of the role that inventory plays in your business. It also works the other way around: the more digitally mature your organization, the easier it will be to implement the perpetual system.

With the affordability of automated inventory management systems, the perpetual approach to inventory has become a go-to option for most companies.

Meanwhile, periodic inventory counts are a good option for certain situations even if your operations are already mature:

High-volume, short-duration selling events where there’s no time to scan each item.

• Clearance or Seasonal Campaigns

Flash sales where manually reconciling afterward is simpler than setting up real-time adjustments across dozens of price points or bundled offers.

• Test Markets or Pilots

When testing a new product, especially at limited locations, a single “period” count lets you evaluate performance without a full-blown integration.

Conclusion

Choosing between a perpetual and periodic inventory system is a strategic decision that affects both your company’s financial accuracy and day-to-day operations.

Understanding the difference between the two starts with the basics of financial accounting, which we covered at the beginning of this article.

If you need real-time tracking and system integration, a perpetual system might be the way to go. But if you’re running a smaller operation or only need to track inventory now and then, the simplicity of a periodic system could be just fine.

Even as technology shifts the standard toward perpetual inventory, understanding both methods gives you the flexibility to choose the right fit for your business—and adapt when things change.

RELATED POSTS